SGD Topside Constrained by Policy with Emerging Convexity

MAS is expected to tighten policy even as geopolitical risks soften. SGD unlikely to significantly rally due to MAS S$NEER band but downside elevated from options positioning

SGD faces an interesting regime going into the July MAS meeting. In this article, I argue that MAS policy is still loose, but unevenly so. This gives them space to tighten as the growth-inflation risks tilt towards price stability amid higher global crude prices. This should result in an S$NEER band steepener at the MAS July meeting. However, this is unlikely to translate to a stronger SGD as it is already near the topside of the band. On the other hand, market makers’ significant short delta exposure to USDSGD means that SGD weakness could be spurred by Gamma pinning.

In short, on a risk-adjusted basis, buying USDSGD on dips is a prudent strategy. SGD-funded carry trades still make sense, but additional buffers should be embedded to account for the rising risk of a weaker SGD.

There will be no TAM posts for the next two weeks as I will be offline

Monetary policy is likely still quite loose

MAS’s next meeting, which should happen before 31 July, is expected to be a live one. But I ultimately think that another tightening is in the cards even as SGD persistently test the top side of the S$NEER band in recent days.

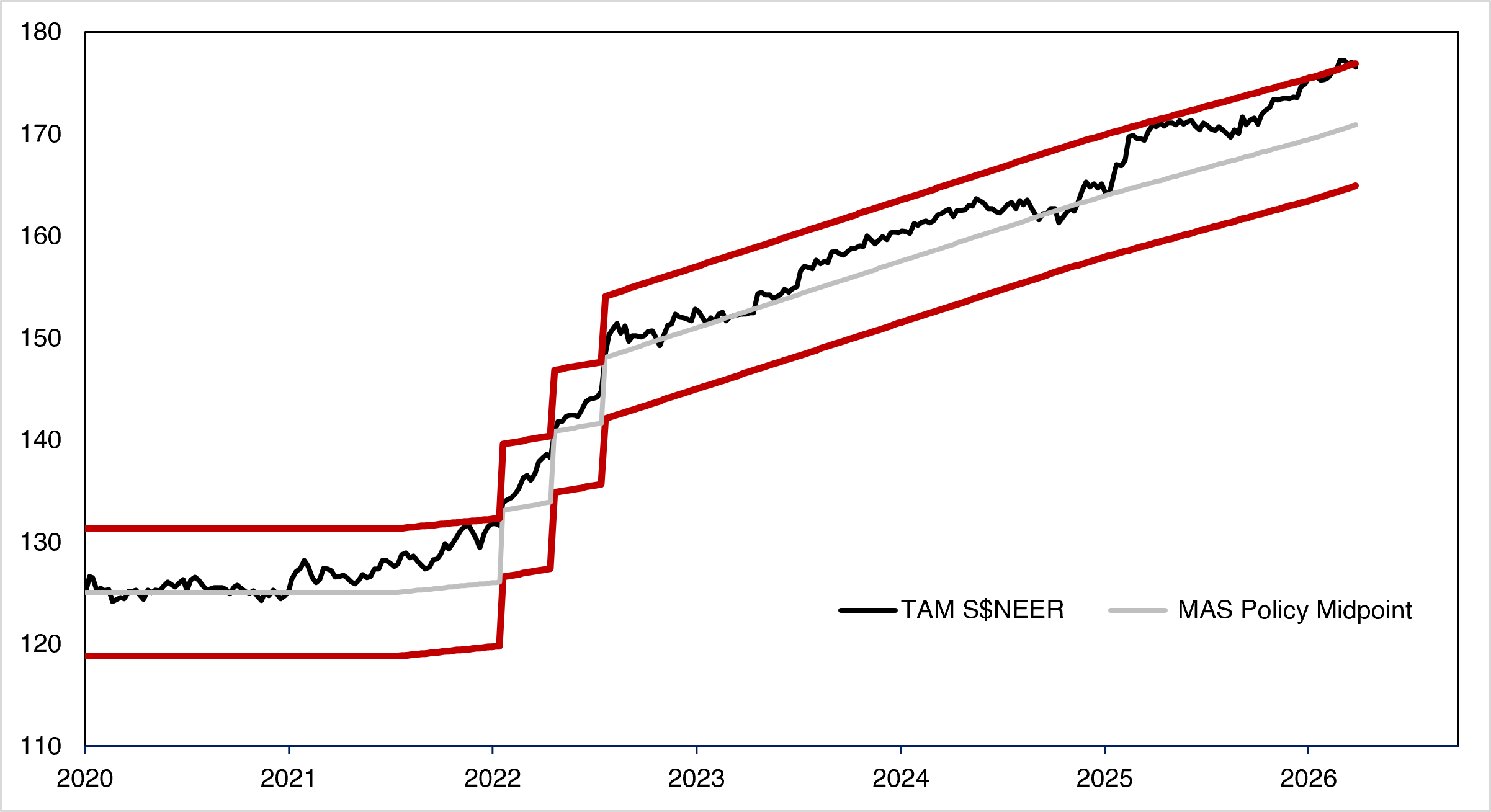

MAS likely steepened the S$NEER policy band in April (perhaps by around 0.5% p.a.), amid the oil price spike during the height of the US-Iran tensions. While framed as a response to rising imported inflation risks, a modest steepening is unlikely to have a meaningful impact on import prices. Rather, it may have been a way to tee up further tightening later while avoiding a more disruptive policy shift.

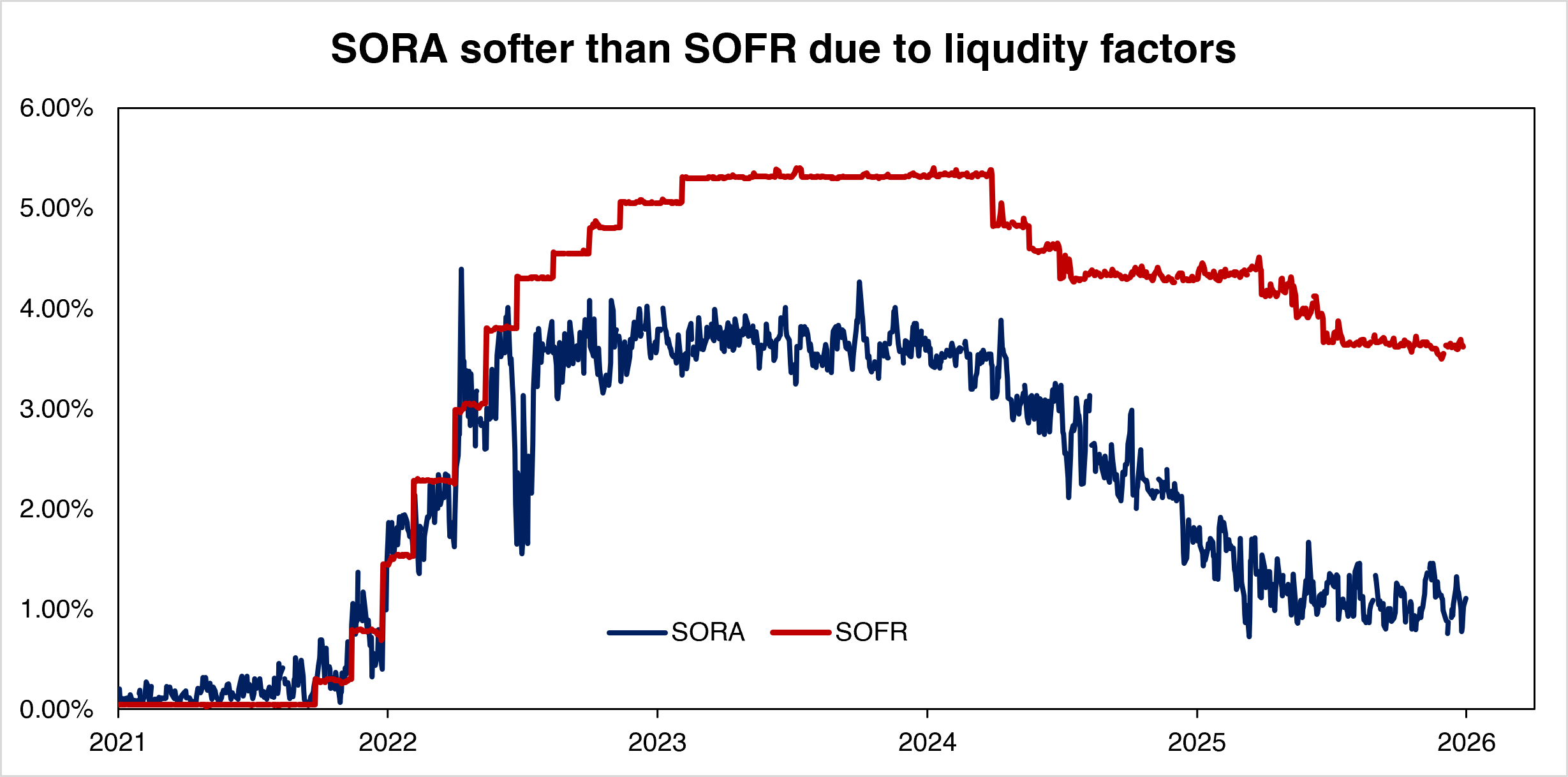

My model suggests the S$NEER has since been pushed aggressively higher, despite MAS continuing to sell SGD into rallies. The associated liquidity injection appears to have been absorbed at the front end, with SORA and MAS Bill yields declining sharply.

Consequently, SORA has fallen well below SOFR, easing domestic credit conditions and reducing borrowing costs in Singapore. As a result, overall monetary conditions remain relatively loose despite the recent tightening in May. Nonetheless, the stronger SGD, driven by a steeper S$NEER path and safe-haven inflows, is likely creating pockets of tighter financial conditions. Exporters may face some pressure from currency appreciation, although lower imported input costs should provide a partial offset.

In short, MAS is far from an overly tight policy and has some room to ease in the coming meetings.

Balance of risk tilts towards inflation

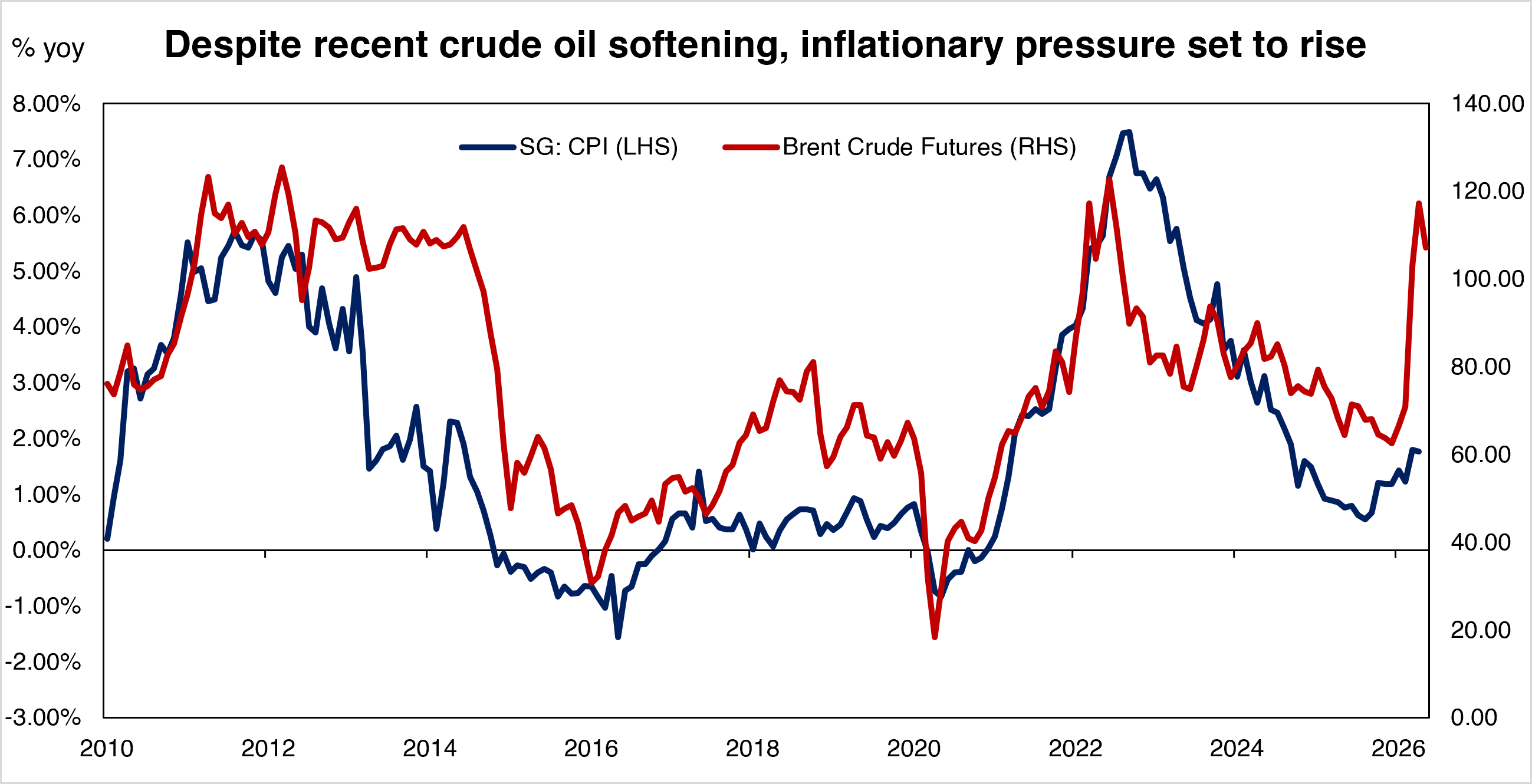

Despite the easing of oil prices in recent weeks due to productive peace talks between the US and Iran, inflation risk is still present in Singapore. There are two major risks to price stability now. First, even as Brent eases from the>USD100/barrel range, easing to around USD80 still represents around 20-30% yoy gains. Second, Singapore’s electricity tariff structure is recalculated every quarter, which means that Q3 and Q4 will experience elevated utility prices.

These effects, alongside the historical correlation between CPI and Brent, suggest that there is significant room for inflation to rise. I would hazard a guess and suggest that, given Singapore’s moderate EV adoption rate, price pressures would broaden beyond energy. Higher logistics costs will likely be passed onto consumers, pressuring goods inflation upwards.

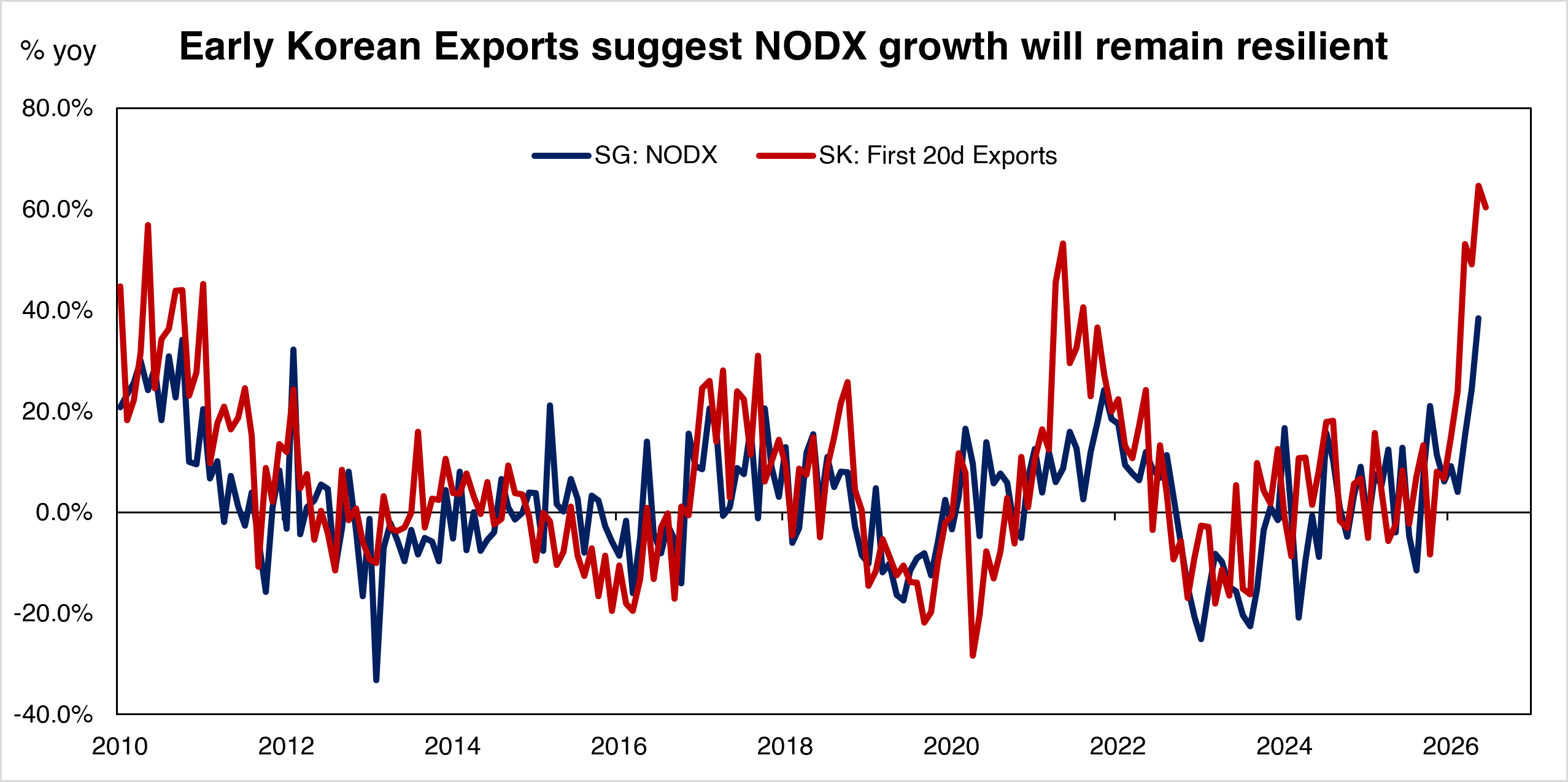

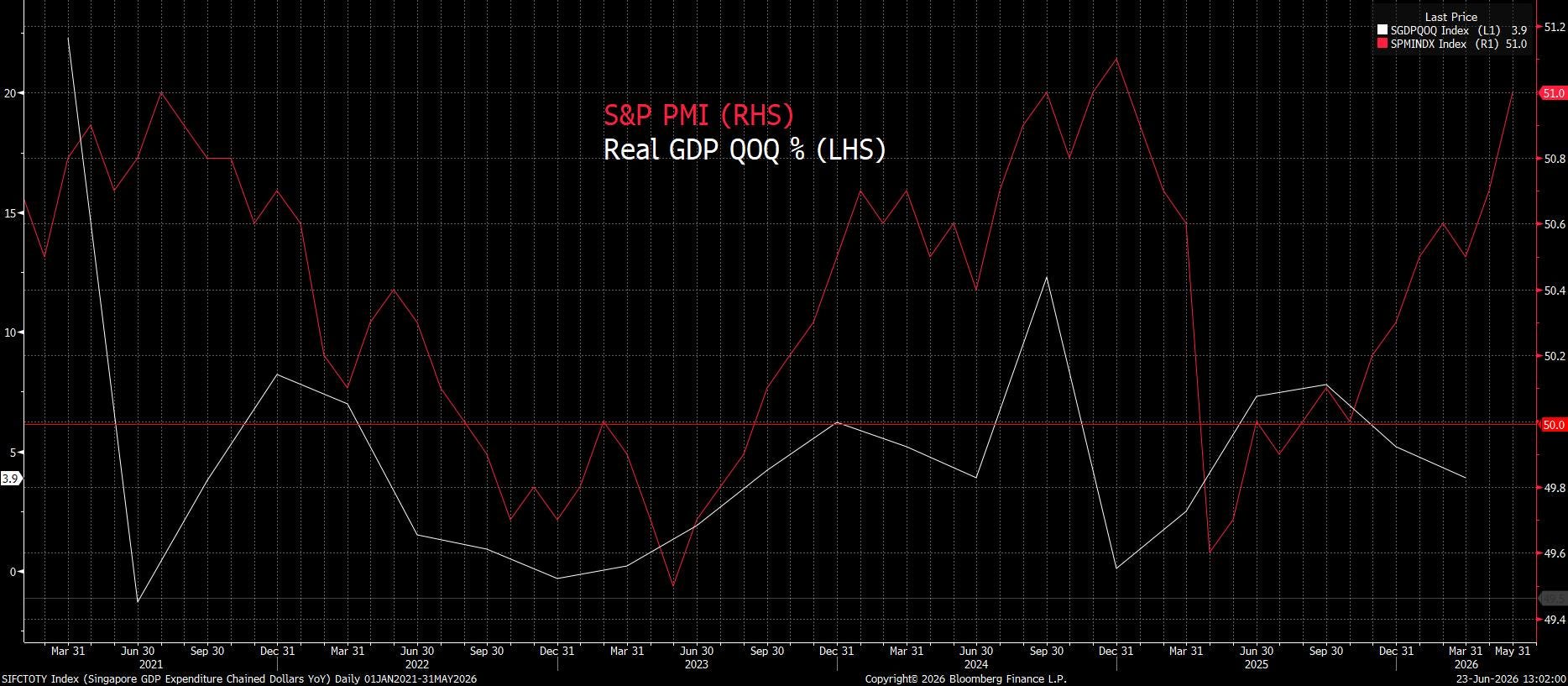

Singapore’s impressive growth (1Q26: 6.0% YoY; 2025: 5.0%) has been driven largely by resilient semiconductor exports. This reflects Singapore’s role in the semiconductor supply chain, particularly in chip-making equipment, wafers, and trailing-edge products such as hard disk drives and legacy logic. As a result, Singapore’s electronics exports tend to track the activity in leading-edge semiconductor hubs such as Taiwan and South Korea.

South Korea helpfully publishes high-frequency trade data, with its 20-day export measure widely regarded as a leading indicator for the regional electronics supply chain and, by extension, Singapore’s exports. This indicator suggests that Singapore’s NODX could accelerate further in the coming months, potentially exceeding 40% YoY growth. An unprecedented level

Policymakers may interpret the strength of recent growth data as evidence that the economy can absorb further monetary tightening. After all, S&P PMI data suggest that headline growth is poised for further gains in the coming months. The risk, however, is that aggregate growth figures overstate the breadth of the expansion. Several sectors with a higher concentration of local workers continue to face softer conditions, suggesting that the benefits of the semiconductor upcycle may not be diffusing evenly across the economy.

Nevertheless, monetary policy is a blunt instrument. From MAS’s perspective, the strength of the semiconductor sector may provide sufficient justification for further tightening if inflation risks remain elevated, even if growth conditions remain uneven across industries.

I believe that MAS will slightly steepen the MAS $NEER band in the July meeting.

MAS Limits USDSGD Downside, Options Positioning Defines Upside Regime

Overall, the SGD has held up well this year, weakening by just 0.7% against the USD year-to-date. Among Asian currencies, only the CNH has performed better, leaving the SGD ahead of both the HKD and MYR.

Prima facie, this suggests that further MAS tightening could drive USDSGD lower. However, both spot levels and options market pricing imply that much of this optimism may already be reflected in the exchange rate, leaving the balance of risks less one-sided than it initially appears.

By anchoring the TAM S$NEER band around spot USDSGD, we can visualise the intervention regions that MAS is likely to operate in. Thus far, it appears that SGD have persistently remained in these regions. Rough estimates suggest that MAS sold around USD5.0bn of SGD assets to maintain USDSGD within the band. With such tight margins, the space for USDSGD to fall further is severely limited

In the near-term, a journey down to the high 1.2700 would require a meaningful number of optimistic moves from FXs in the MAS S$NEER baskets to pull the band lower. 1.2800 is the near-term floor with some space for the pair to fall towards 1.2750 on a 3-6 month horizon.

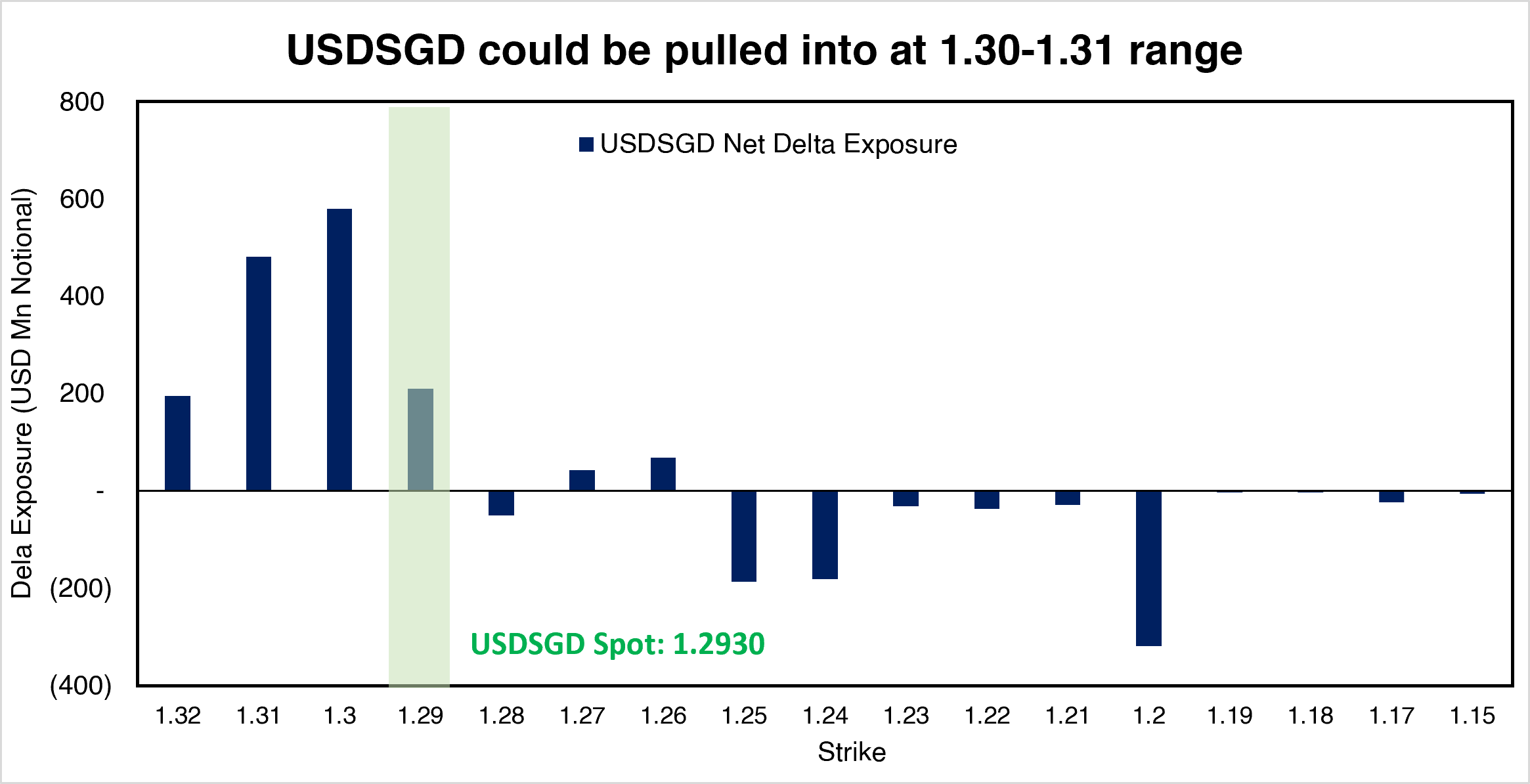

This crowded positioning may create a pinning effect around the 1.30-1.31 range. Because market makers typically take the opposite side of client flows, widespread demand for USDSGD topside protection implies that dealers are short delta in this area. To remain delta-neutral, dealers hedge this exposure by buying USD against SGD.

The mechanics become more important as spot approaches the strikes where positioning is concentrated. As USDSGD rises towards 1.30, the delta of these options increases, causing dealers’ short delta exposure to grow. To maintain a neutral book, dealers must buy additional USD. The closer spot moves to the strike, the faster delta changes, forcing dealers to buy progressively larger amounts of USD. This creates a source of incremental USD demand that can reinforce moves in the exchange rate upward.

However, these flows are most influential near the strike. Once USDSGD moves decisively through the largest concentration of exposure, dealer hedging can become self-reinforcing as option deltas rapidly approach one. In this scenario, the 1.30-1.31 region transitions from an area of concentrated positioning into a potential acceleration zone, where hedging flows amplify rather than dampen moves in spot.

A steeper S$NEER path would reinforce the structural floor for SGD, but should not be read as a catalyst for further appreciation. With USDSGD already within 0.45% of the implied upper bound, a 0.5% p.a. steepener only adds 0.1-0.2% of additional headroom, insufficient to shift the balance of risks meaningfully. The more consequential implication of further tightening is that it anchors the floor, not that it opens new topside for SGD.

In short, the path of least resistance is a topside adjustment, with a clean break and a daily close above 1.30, which could trigger an acceleration through 1.31 as market makers square their hedges. MAS policy keeps downward risks for USDSGD constrained, leaving a structural floor for any pullbacks. This makes risk-rewards asymmetrically biased towards long USDSGD on dips.

The US could be the catalyst for USDSGD to rise

A stronger USD could be the catalyst that pushes USDSGD towards the 1.30-1.31 options-heavy zone.

I see two potential drivers. First, uncertainty surrounding the US-Iran ceasefire remains elevated. As discussed in a previous Markets This Week update, the peace framework appears fragile, and any renewed escalation could quickly revive demand for safe-haven assets such as the USD. Second, the Fed appears to be maintaining a relatively hawkish stance. With inflation still above target and policymakers offering less forward guidance, markets are likely to remain sensitive to upside inflation surprises and the possibility of a higher-for-longer rate path.

SGD-based investors should therefore be mindful of the risk of a temporary spike in FX volatility over the coming weeks. In practical terms, SGD-funded carry trades remain attractive, but investors should ensure that the return on the investment leg comfortably exceeds the potential FX drag from a move towards 1.30-1.31. A yield buffer of roughly 60-80bp appears prudent. That said, absent a significant macro catalyst, volatility is likely to remain relatively contained as investors continue to favour defensive positioning over aggressive risk-taking.